Depressed Consumers or Living Their Best Life?

Depressed Consumers or Living Their Best Life?

What is the state of the consumer telling us about the second half of 2024

The big question for investors and businesses alike is the state of the economy and what the Fed is going to do next. Last year the markets were expecting a whole lot of rate cuts in 2024 that have now been pushed back to fewer and later. To understand what is coming next, let’s look at some indicators for the state of the consumer.

If you have taken a vacation over the past few years (and according to my Instagram feed, literally everyone is going somewhere fabulous, “living my best life”), you have likely been made mental noticed the insane number of people around you doing the same. You may have heard how the staggering number of tourists in Venice is causing the city so many problems that it charges tourists entry fees for short stays. Where I live a good portion of the year, in Lake Como, is planning to do the same. The change in the sheer volume of tourists in Como from 2019 to today is mindboggling.

How the world suffers through a historic health crisis and then experiences skyrocketing tourism isn't exactly obvious.

To recap, the global health crisis decimated supply chains, which pushed governments to open the money spigots to full blast, creating a massive explosion in demand while many couldn’t go to work. When stuck at home, what else do you do but shop online and buy a Peloton? Demand surged while supply crashed, shocking that stuff cost more—inflation.

Then there are those trade wars. Add in an invasion of Ukraine, the war in the Middle East, and pirates attacking ships along crucial supply chains. Put that all together, and you get a significant push for onshoring/near-shoring of production, and the supply side of stuff continues to be complicated.

It is not hard to see why things got so expensive, but what about all that holiday travel? How?

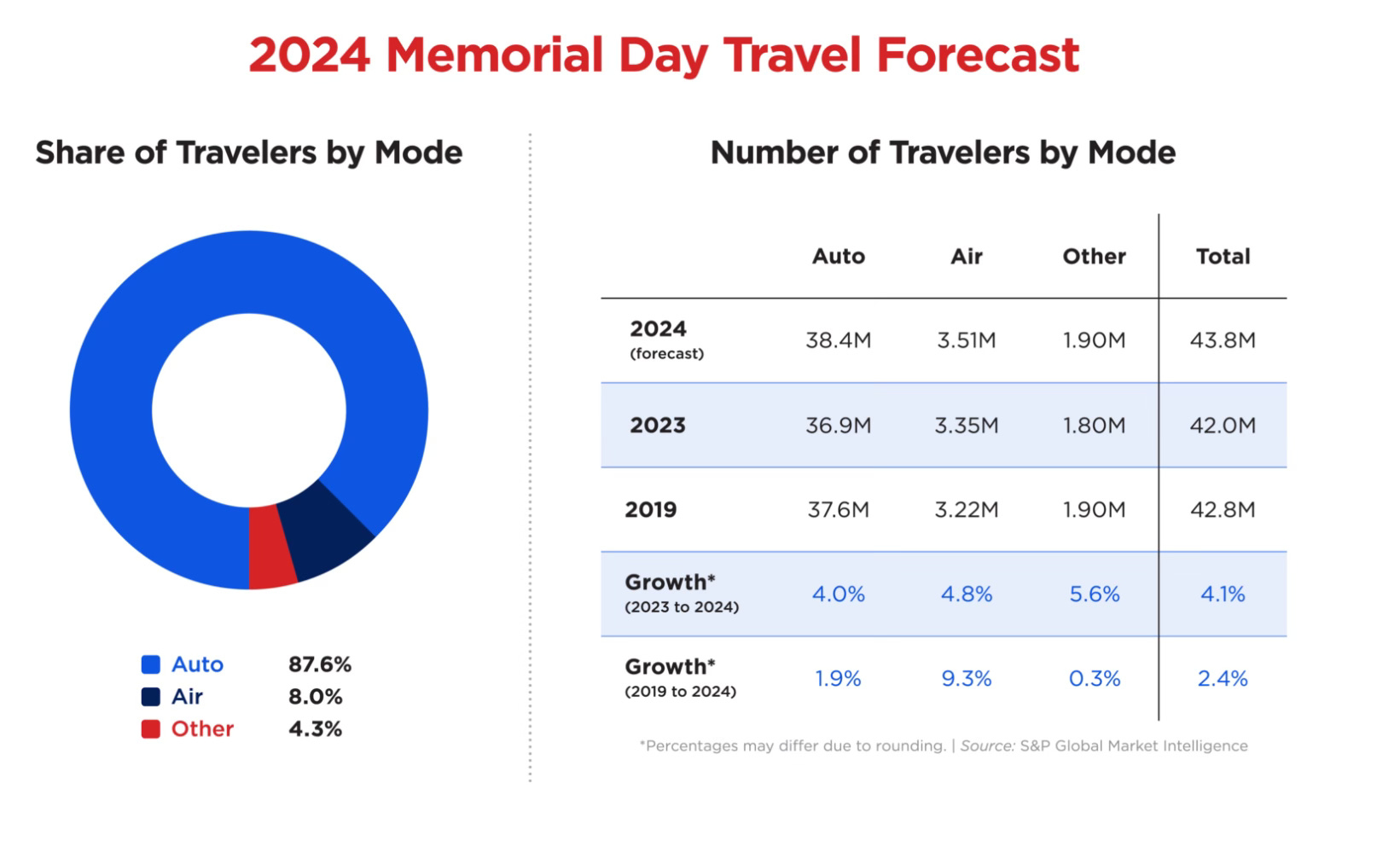

According to S&P Global Market Intelligence, 2024 Memorial Day was expected to see travel numbers, unlike anything we’ve seen over the past two decades, with an additional one million travelers this past weekend compared to 2019, signaling a hectic summer travel season.

AAA expects an increase of nearly 5% in air travel over last year, up 9% from 2019. The number of travelers driving 50 miles or more from home over the weekend was expected to be 4% higher than last year, nearing 2005’s recording of 44 million.

It isn’t just Italy that’s seeing a lot of tourists.

So, how is this happening?

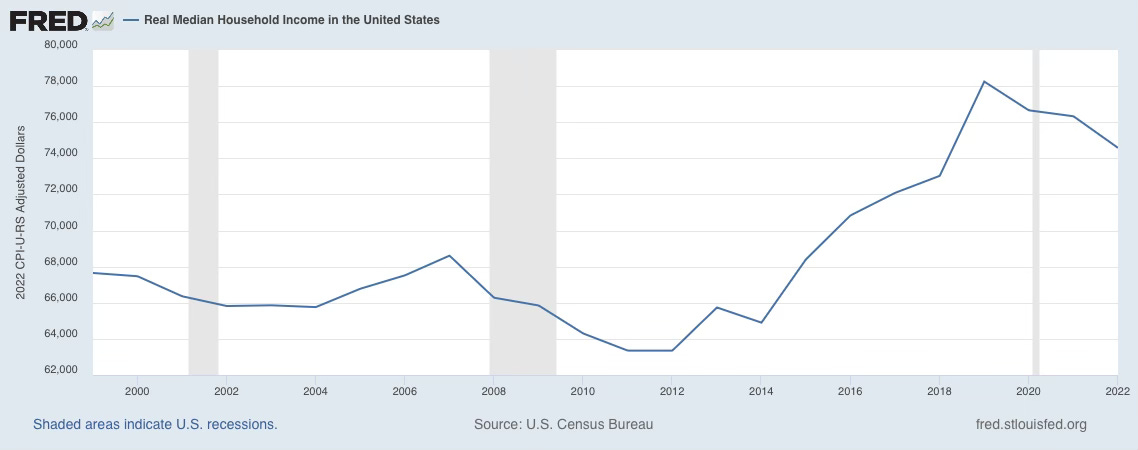

From 1999 to 2015, real median household income barely changed, but from 2012 to 2019, we finally got some traction and rose 23.5%. But from 2019 to 2022 (the latest data available), it has fallen nearly 5%. So we were doing pretty good before heading into the pandemic, but incomes have been falling since then.

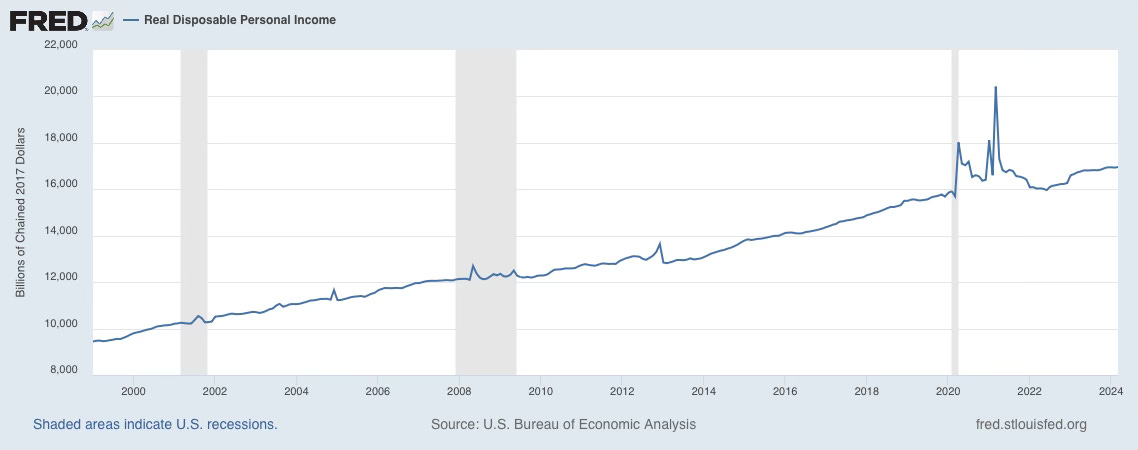

Real disposable personal income paints a similar picture, rising just 7% from the start of 2020 to March 2024, about a 1.6% increase yearly.

How can travelers afford these “living the life” trips?

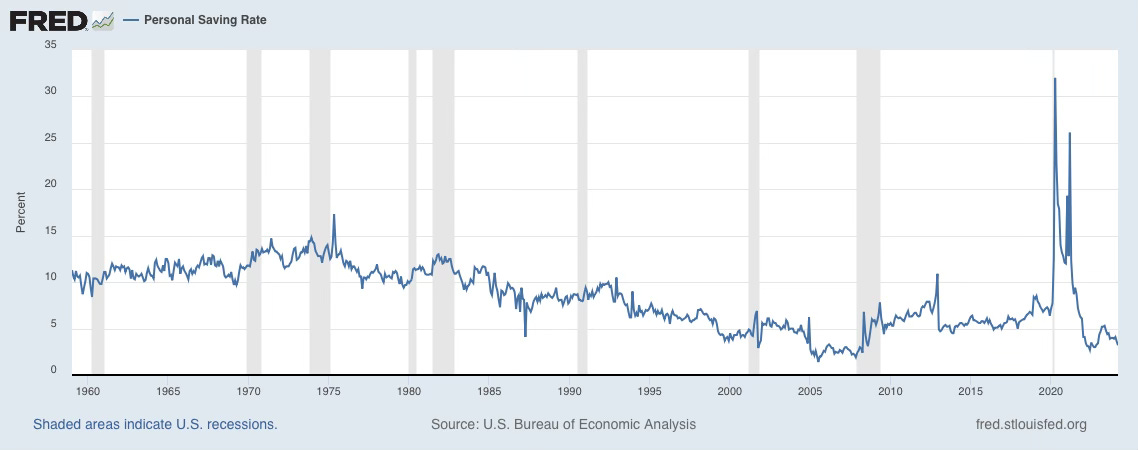

One is taking away from savings. For a historic perspective, from 1960 to the mid-1980s, the savings rate remained around 10%. It fell from the early 1980s through the Great Financial Crisis, bottoming at 1.9% in November 2007. Savers regained their enthusiasm somewhat, with a median savings rate of 6% between 2010 and the end of 2019. Savings then got wacky high when so many people were stuck at home, and there was a mortgage and student loan moratorium. However, since the end of the pandemic, the savings rate has been moving back down, with a median rate of just 3.9% between January 2022 and March 2024, when the rate dropped to 3.2%.

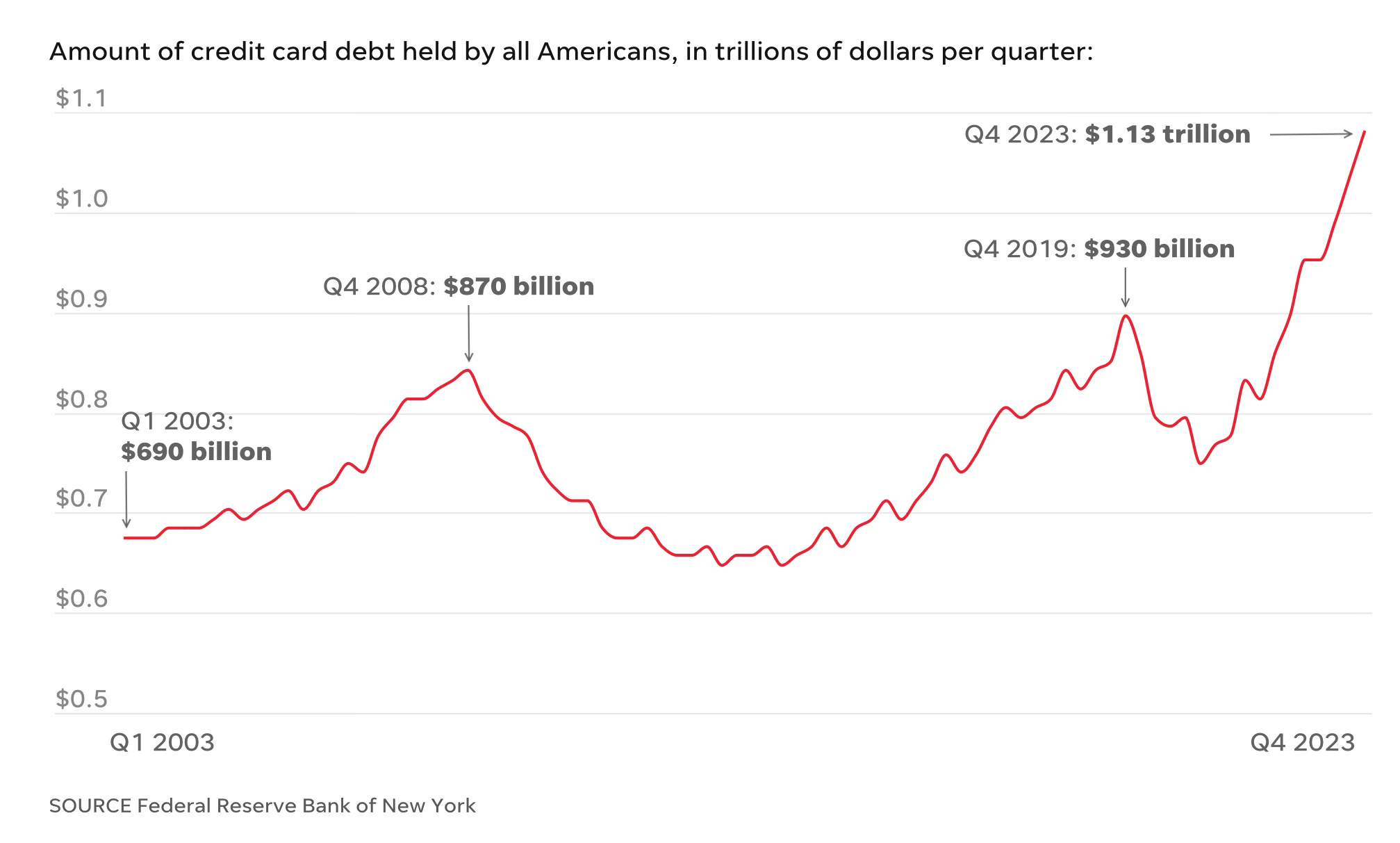

The real kicker is credit card debt, which skyrocketed to a record high of $1.13 trillion in Q4 2023. There you have it, living the life using the card.

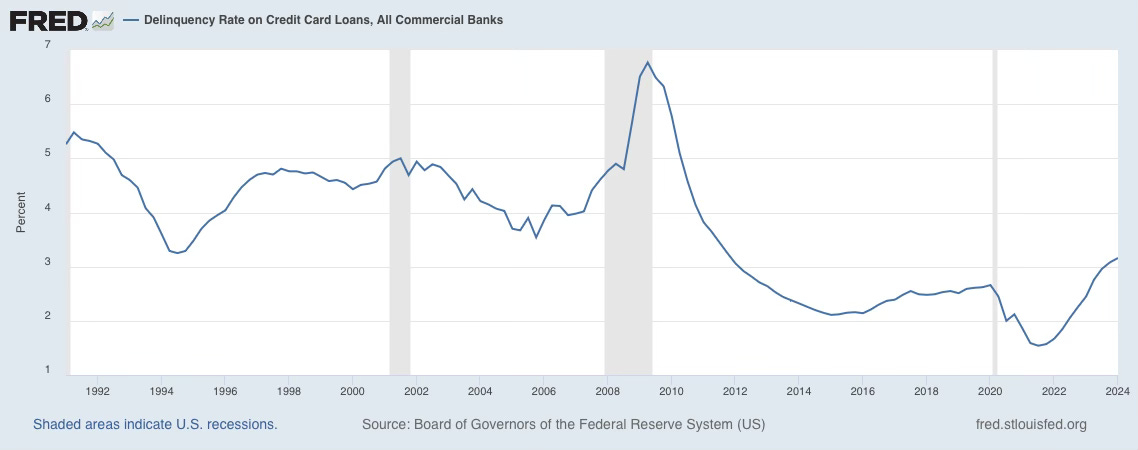

The good news is this isn’t a significant problem yet, with credit card delinquencies still low by historical standards, but the rate of increases is concerning.

So just how is the American consumer feeling these days?

A recent Guardian/Harris poll has 56% of respondents say they believe the US is already in a recession with 58% blaming President Biden - not great six months before the election.

The Wall Street Journal ran an article last week about Jeep and Ram dealers griping to Stellantis about weak sales and rising inventory levels.

This earnings season, retailers, restaurants, and almost every other consumer-related company have expressed concerns about weakening demand. Walmart, Target, Aldi, and Amazon Fresh have all announced price cuts to attract the more frugal consumer.

McDonald’s and Burger King are launching value meals as Americans cut back on eating out. A recent LendingTree survey found that 78% of respondents consider fast food a luxury.

The latest University of Michigan Consumer Sentiment Survey reveals consumers are much less willing to buy.

The share of people who say now is a good time to buy big-ticket items dropped to 40% from 51% in March and April. That is a level below what we saw before the last five recessions.

Homebuying intension plummeted to a record low of 28 in May from 50 in March.

More than half of respondents don’t think they will receive a wage increase in the coming year, and 38% expect the unemployment rate to rise.

As for that stellar labor market, according to the National Association of Colleges and Employers, new hiring for the Class of 2024 is down 5.8% from last year.

The Bottom Line is that it is getting pretty late for the post-pandemic party at a time when the S&P 500 PE ratio has risen to 20.8x from 17.5x last October. The current PE level is more than 30% higher than is typical at today’s interest rates. The economics of the consumer is weakening, retail prices are leveling off, and hiring is slowing. The Fed, as always, will lower rates too late just like it raised too late, most likely right around when the last bond investor throws in the towel.