Inconceivable Inflation and Inigo Montoya

Inconceivable Inflation and Inigo Montoya

These days, investing markets focus on one word above all others - inflation.

Thursday, things got bizarre with the European Central Bank. It cut its benchmark deposit rate by 25 basis points (as expected) from 4.0% to 3.75% and, at the same time, increased its core CPI estimate for 2024 and 2025 to 2.8% and 2.2%, respectively. That particular dance move was unexpected - simultaneous higher inflation and less restrictive policy?

The truth is we are in unprecedented times with no historical playbooks from which to model likely scenarios. We also have a problem with the word “inflation” itself.

Its meaning is highly dependent on who uses the term and in what context.

Example 1

If oil production is meaningfully reduced, the price of oil will go up, putting upward pressure on prices across the board because oil is a factor for basically everything, from making things to transporting them. When prices across a wide range of products and services rise as a result of a decrease in the supply of just one thing, many will call that inflation.

Example 2

If we learn that eating two kumquats a day cuts the risk of cardiovascular disease and cancer by 90%, the demand for kumquats will skyrocket, and so will the price. Perhaps the price of a few kumquat-adjacent fruits may also be affected by sheer association. Land in areas where kumquats grow will certainly get more expensive, but overall, it will not have a massive impact on the economy. In this case, prices also go up, but it won’t be called inflation.

Example 3

You and nine friends set sail on what is supposed to be a 3-hour tour. Instead, the ship goes through a wormhole and you are shipwrecked on a remote island in an alternate universe. On this island, a fixed number of bananas and coconuts grow, and a fixed number of fish can be caught annually. You find a chest of gold on the boat and divide it amongst everyone to use for currency so that some can specialize in fishing and others in banana and coconut harvesting. Given that the number of things to eat doesn’t change from year to year, prices are stable. One day a passenger-less ship emerges through that same wormhole filled with gold, again divided among everyone. Nothing else has changed, just the amount of gold, so the price of a banana in gold will increase. Milton Freidman would definitely call that inflation.

Pandemic Punchbowl

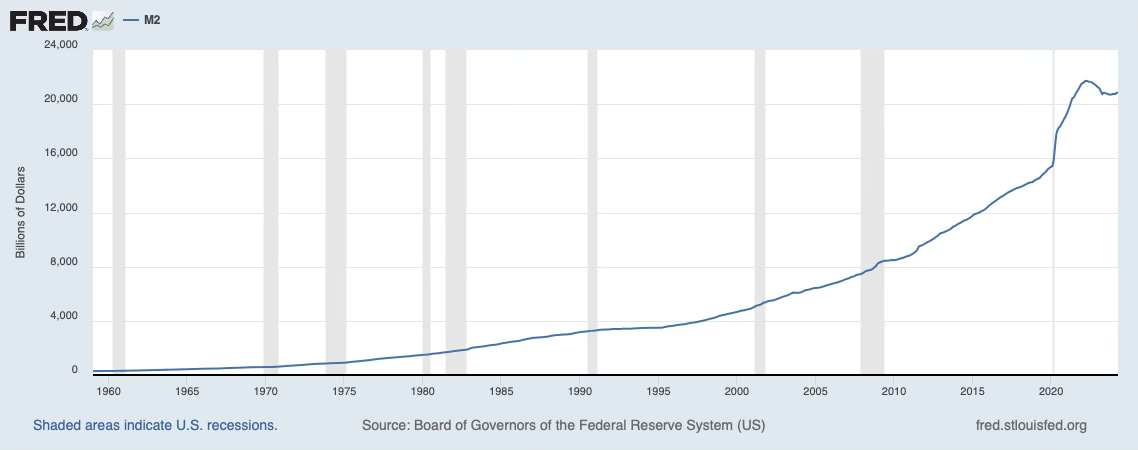

Speaking of gold showing up out of nowhere, look at what happened to the money supply as measured by M2 during the pandemic. The Federal Reserve considers M2 to include all of M1 (which includes cash, checkable (demand) deposits, and savings) as well as time deposits, certificates of deposit (CDs), and money market funds.

M2 rose from $15.381 trillion in January 2020 to $21.722 trillion in April 2022. That is an increase of 30% of 2019 GDP, which was $21.381 trillion

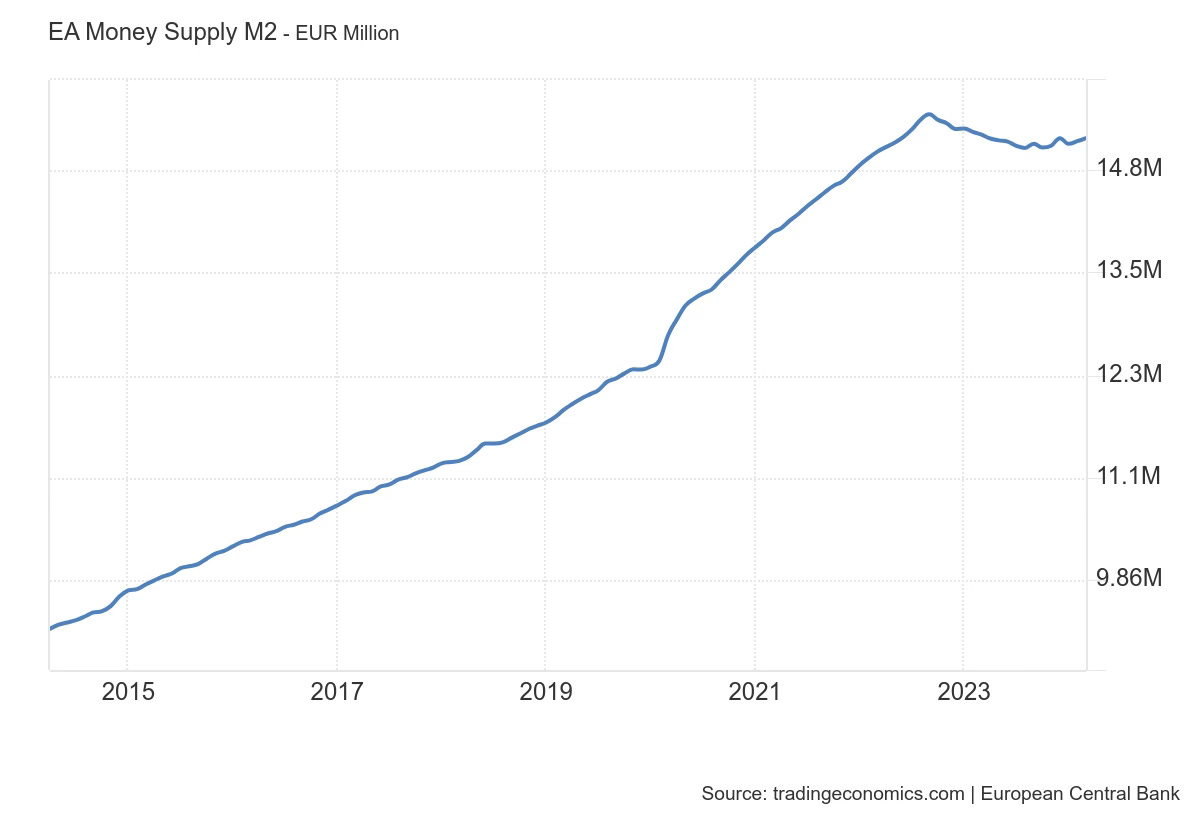

In contrast, M2 for the euro rose from €12.4 trillion to a peak of €15.4 trillion, an increase of 22.3% of 2019 GDP.

The increase in euro liquidity was less than 3/4th that of the US dollar.

Think about that when you hear how the US economy is so much stronger; it is like comparing energy levels after a shot of espresso versus a shot of adrenaline directly into the heart.

With either metric, the increase in the supply of money was an enormous percentage of the economy, making inflation inevitable. On top of that, lockdowns slammed supply while demand for things like a new couch skyrocketed.

But here is where it gets complicated. The money supply has skyrocketed to an unprecedented degree, so prices were obviously going to have to rise, but the change in prices has been anything but homogeneous.

Inflation By Any Other Name

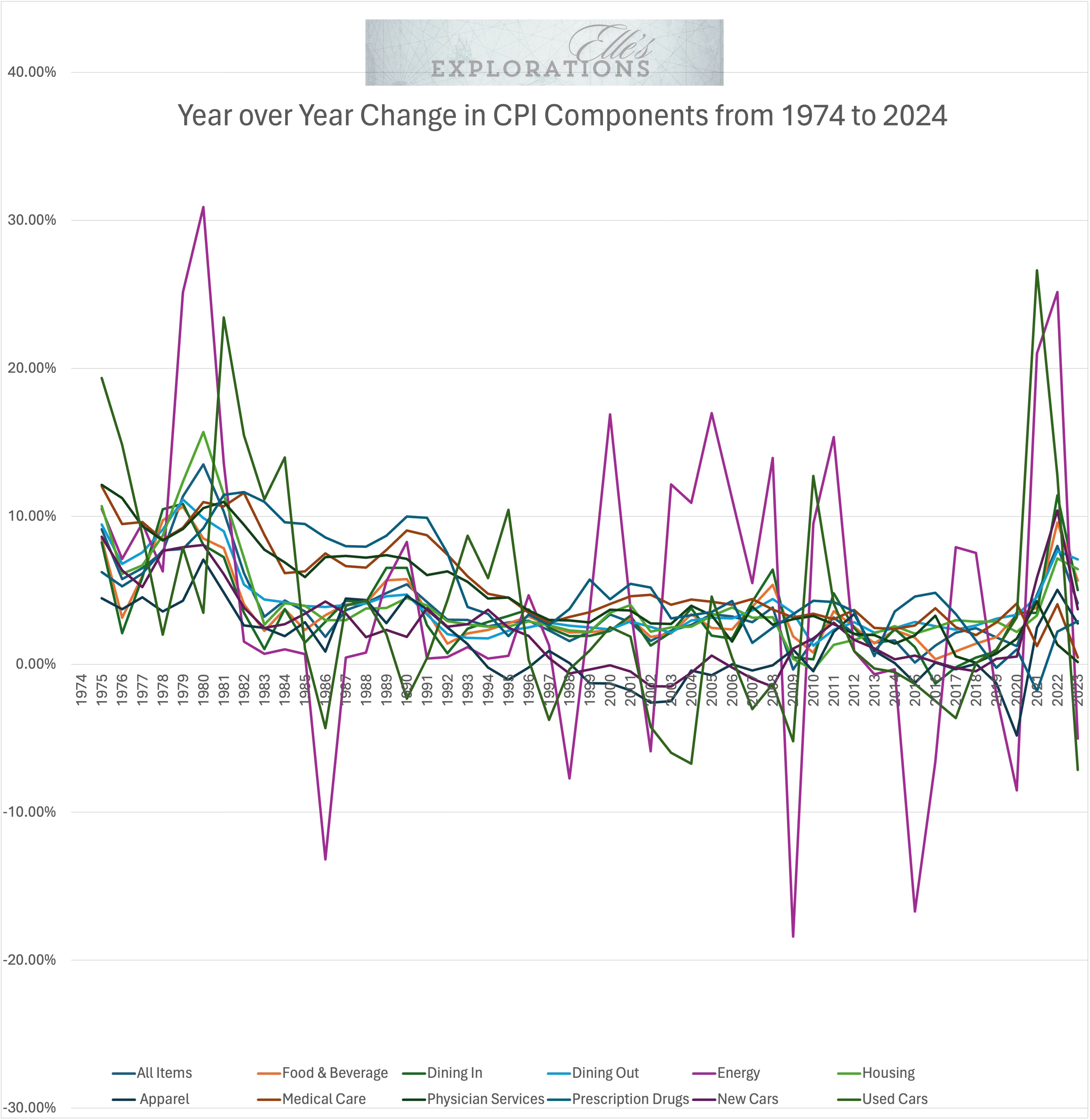

This horribly ugly chart shows the change in CPI for a select group of components, including energy, apparel, housing, prescription drugs, and new and used cars.

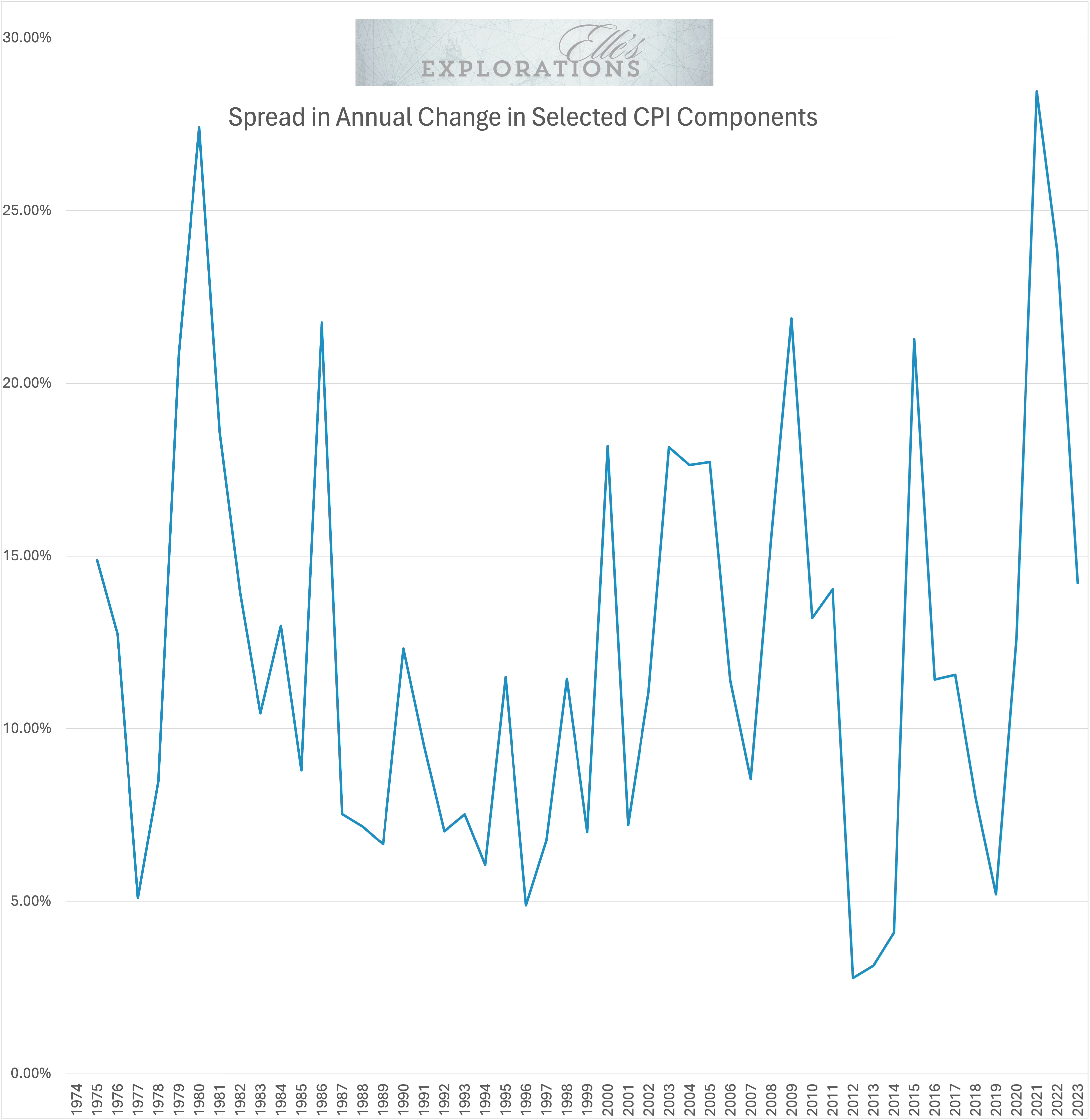

The main takeaway is that energy fluctuates the most, followed by used cars and prescription drugs. This next charge shows the range between the biggest and smallest annual change in CPI amongst these components. In 2021, the divergence in inflation reached a new record high. Used car prices rose 26.6% year-over-year, while prescription drug prices fell 1.8%.

So the problem becomes how do you measure it? The St Louis Fed recently published a piece on just this, but to summarize with some much-needed snark, here are the primary metrics the Fed watches:

Consumer Price Index (CPI)

Personal Consumption Expenditures price index (PCE)

CPI and PCE are similar, but CPI is more accurate for urban consumers, while PCE is broader and is less impacted by housing costs.

Then there are the “core” versions of both of these, which remove the cost of energy and food because who really buys gas, electricity, and food? The prices of these tend to be a lot more volatile, so an argument can be made, but excluding them really discounts what the consumer is actually experiencing.

Next, the Fed introduced “super core.” This one subtracts the same as core - food and energy - and also excludes shelter. So, basically, they remove the three items that account for nearly the entire budget of most people. Sounds reasonable. This logic was because the price of housing is now considered too volatile.

The intention with these adjustments isn’t to more accurately describe what has already happened but rather to predict what is coming next. As I pointed out earlier, the differences in the price changes across spending categories have reached a record high, so assessing inflation over the past year and trying to predict where it will go next is, in many ways, harder than ever. Particularly given that there is absolutely no historical playbook from which we can develop a mental model. We just haven’t ever been here before, so what happens next is really hard to predict - be wary of anyone who claims it is easy.

We’ve never had the world’s global reserve currency dump this much liquidity into its economy so fast at a time when global production was decimated, supply chains a wreck, and social media was available to remind everyone how much they were not “living their best life.”

As I wrote about earlier, the output gap is widening and likely to continue widening, putting downward pressure on prices. The pandemic-induced remodeling, traveling, and overall “living my best life” spending spree has pushed credit card debt to record levels, and defaults are rising. Credit card default rates aren’t anywhere near panic levels today, but this conversation would be too late if they were. What concerns me is the rate of change rather than the absolute level.

The next thing to watch is mortgage refinance applications. Home prices have skyrocketed over the past few years, and cash-strapped consumers may pull equity out of their homes to support their spending and accumulated debt. Clearly, today’s mortgage rates make that a really bad idea, as for most, it will mean paying a meaningfully higher rate, but it is a lot easier to borrow to keep up spending than to shift to frugality. Just ask a politician.